How Mints Will Be Affected by Surging Bullion Coin Demand

JP Koning

JP Koning 3 Comments

3 CommentsWith the coronavirus sweeping across the globe, the demand for gold and silver coins as a hedge has exploded. BullionStar, for instance, has experienced “extreme" demand for precious metals over the last month. This race to precious metals has caused bullion coins to trade far above their intrinsic metal content priced at the spot price.

For instance, BullionStar recently announced that is it willing to buy Silver Eagle coins at a 25% premium to the spot price of silver. Spot prices for silver and gold are predominantly established at the trading venues of the COMEX futures exchange in the U.S. and the LBMA market in London.

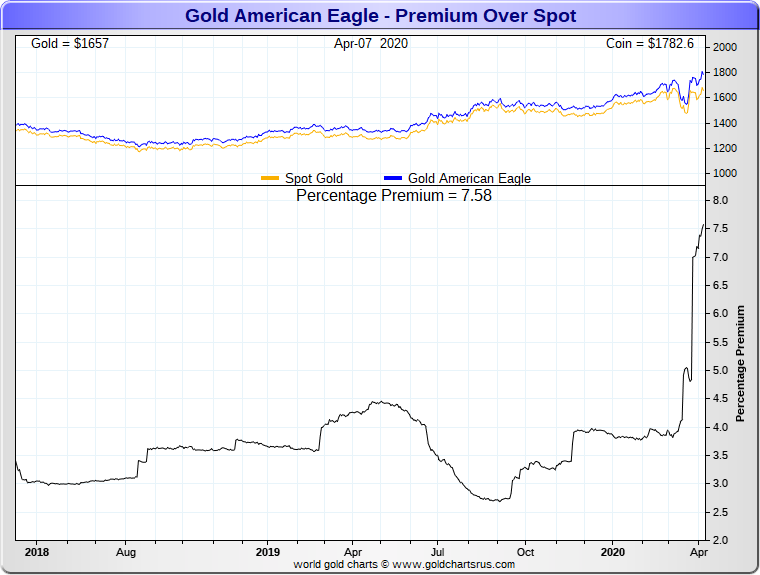

Below is a chart of the coin premium for Gold Eagles. They are currently trading at a 7.5% premium to spot at various bullion coin dealers.

Bullion coins are produced by both private and state-owned mints all over the globe. In this post I want to explore how this increase in consumer demand for precious metals will flow through to mints. To what degree will their profits be affected?

A tough few years

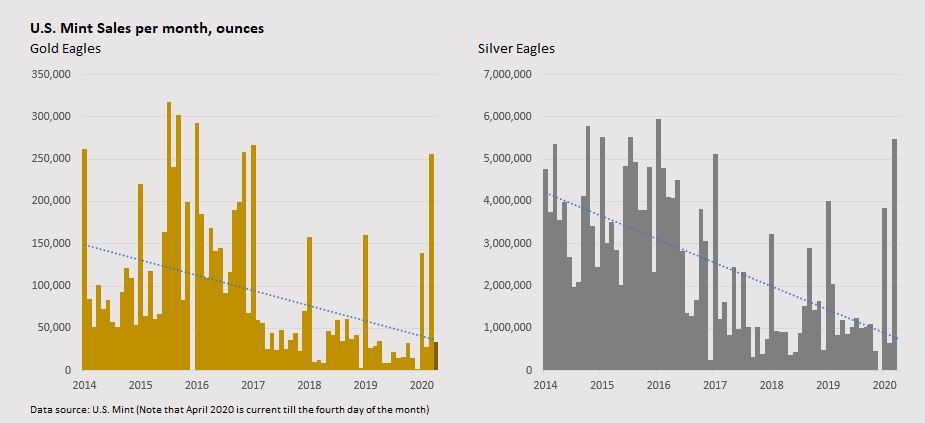

The increase in consumer demand for gold and silver coins first shows up at bullion dealers like BullionStar. As dealers run down their stocks, they must turn to the various mints for new supply. One the world’s most popular precious metal coins is the Eagle, which is produced by the U.S. Mint. In the chart below, you can see that the U.S. Mint’s sales of both gold and silver Eagles have exploded over the last month as dealers submit purchase orders to the U.S. Mint in order to replenish their stocks.

As the US Mint’s inventories are depleted, it will have to ramp up bullion coin production in order to meet demand. Note that the U.S. Mint’s big increase in sales this March (and what looks to be a massive April, assuming it can maintain production levels and restock in time) has come after a few difficult years. Bullion coin sales show a declining trend in the above charts.

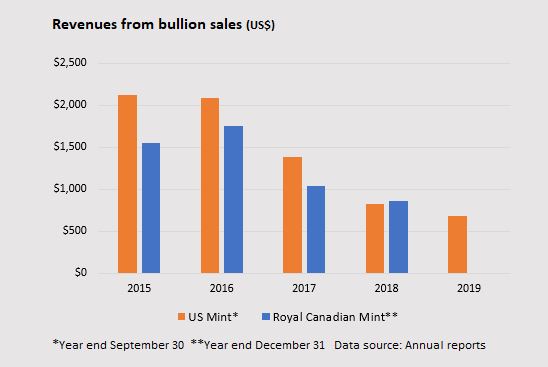

The U.S. Mint isn’t alone in experiencing a slowdown. The Royal Canadian Mint, which produces the popular Maple bullion coin, has also suffered through a period of lean coin sales. Below I’ve charted bullion product revenues for both the Royal Canadian Mint and U.S. Mint going back to 2015 in US dollar terms. This includes revenues from both gold and silver coins.

Minting gold is a low margin game

Producing and selling precious metal coins is a low margin business. That is, the amount of profit that a mint can earn for each bullion coin is pretty small.

The reason for this is that a bullion coin is really just a round of gold or silver with a stamp on it. A mint’s stamp is valuable because it serves as a guarantee. But there are limits to how much people will want to pay for a stamp. After all, they can always get a gold bar or even raw gold bullion instead.

The U.S. Mint, for instance, sells gold Eagles to authorized dealers at a 3% markup to the spot gold price. Out of this razor-thin markup the Mint has to pay the costs of buying bullion, running the coin presses, salaries, and more.

To illustrate how low margins get in bullion coin minting, here are some figures. In 2018, the Royal Canadian Mint sold US$800 million worth of gold & silver coins. It made a pre-tax profit of just $20 million on that amount. That’s a wafer-thin 2.5% profit margin.

As for the U.S. Mint, it had an even tougher time squeezing profits out of bullion products. The U.S. Mint sold $682 million worth of precious metals coins in 2019. But it made just $5.6 million in profits on those sales, a profit margin of just 0.8%. Ouch.

What about small change?

Luckily for the U.S. Mint and Royal Canadian Mint, they have other lines of business to compensate for low bullion margins. The chief of these is to manufacture regular, or circulating, coins. And circulating coins can be incredibly profitable (I’ll explain why later) to produce. By regular coins, I mean the dimes or nickles that we get back as change when we visit the grocery store.

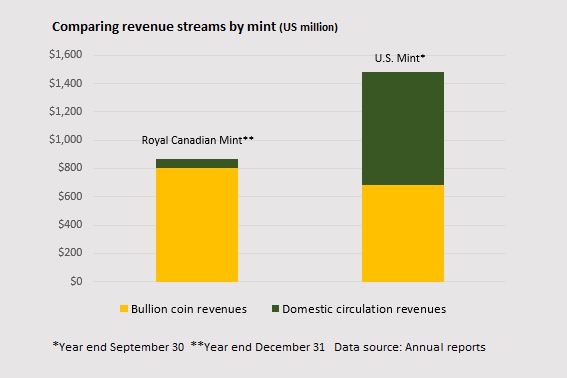

To see how profitable circulating coins can be, let’s begin by comparing how much revenue the U.S. Mint and Royal Canadian Mint make from their bullion and circulating coin businesses. Whereas the U.S. Mint sold around $682 million in bullion coins last year, its circulating coin business brought in $798 million in revenue. So the two lines of business are about the same size. See chart below.

The Royal Canadian Mint, by comparison, received a much smaller revenue stream from the Canadian coins it produces. Whereas its bullion business recorded revenues of US$800 million, it reported domestic coin revenues of just US$68.4 million. That’s a tenth the size of the US Mint’s circulating coin revenues.

There are a few reasons why we’d expect Canadian circulating coin demand to be much smaller relative to U.S. coin demand. Canada is about a tenth the size of the U.S. Furthermore, U.S. coins circulate widely all across the globe, whereas Canadian coins are only valued in Canada.

On the other hand, there are reasons to expect Canadian circulating coin demand to be higher than in the U.S., at least on a per-capita basis. Canadians rely on $1 and $2 coins, whereas the U.S. doesn’t. While the U.S. Mint does issue a $1 coin, the $1 paper note, produced by the Bureau of Engraving and Printing, is far more popular.

Now let’s look at how much profits the two mints earned from their domestic circulating coin programs. On revenue of $798 million, the U.S. Mint earned a massive $318 million profit. That’s an incredible 40% profit margin! With profits like those from minting quarters and dimes, who cares about its tiny bullion margins.

The Royal Canadian Mint earned just $2.6 million on circulating coins, a profit margin of 3.5%. Compared to the US Mint’s 40% profit margin, that’s not too great. Why are Canadian circulating coin margins so low?

Profiting from nickles and dimes

To understand why, let’s explore what drives circulating coin profit margins. The U.S. Mint receives circulating coin revenues by selling dollars, quarters, dimes, nickels, and cents to the Federal Reserve, the U.S. central bank, at face value. The Fed in turn distributes these coins to private banks, which push them into the economy. So the U.S. Mint sells four quarters to the Fed and gets $1.00 back.

To manufacture a coin, the Mint has to purchase zinc, copper, and nickel. Blank discs must be created and then stamped on each side. The coins must then be sorted, packaged, and shipped.

In most cases, it only costs a the U.S. Mint a fraction of face value to produce a given coin. The U.S. quarter-dollar, for instance, cost just 9 cents to produce and distribute in 2019. The Mint sells this 9 cent metal disc to the Fed for 25 cents, meaning that the remaining 16 cents is pure profit. For each four quarters its sells to the Fed, it makes an incredible return of 64 cents. That’s a 64% profit margin!

Whereas the U.S. Mint sells each coin it produces at face value, I suspect that the same does not apply to the Royal Canadian Mint. The Royal Canadian Mint produces coins and then sells them to the Department of Finance, the branch of the Federal government that is responsible for Canadian economic matters. The Department of Finance in turn sells the coins to banks.

I suspect that the Royal Canadian Mint is probably selling coins to the Department of Finance at less than face value. So it is selling four quarters from something like fifty or sixty cents.* And this reduces its revenues, and thus its profit margins. That’s why it earns a miserable 3.5% margin on domestic coinage.

Minting for foreign governments

However, the Royal Canadian Mint makes up for its low domestic circulating coinage margins by selling circulating coins to foreign governments. Many governments don’t have their own national mints, and so they must either hire a private mint or another national mint to produce their coins. Thus the Royal Canadian Mint produces coins for countries such as Madagascar, Indonesia, Jamaica, and United Arab Emirates.

In 2018, the Royal Canadian Mint earned US$67.8 million in foreign circulating coin revenues. Profits amounted to US$12.1 million, far higher than domestic circulating coin profits, for a splendid profit margin of 17.9%.

The big difference in profit margins is probably due to the fact that the Royal Canadian Mint sells coins to the Canadian Department of Finance for less than face value, but sells them to foreign governments at face value. So its revenue per coin is much higher on its foreign business, as are its profit margins.

The U.S. Mint typically doesn’t make coins for foreign countries. The largest producer of circulating coins for other countries is actually the UK’s Royal Mint. Like the Royal Canadian Mint and U.S. Mint, the Royal Mint manufactures both domestic coinage and bullion coins, in the latter case the Britannia (which isn’t quite as popular as either the Maple or the Eagle). In addition, the Royal Mint produced around 3.3 billion foreign circulating coins in 2018. This exceeded the Royal Canadian Mint’s 1.8 billion foreign coins by a wide margin.

More on the U.S. Mint’s seigniorage

The U.S. Mint provides an incredibly broad amount of information in its annual report. This allows us to drill down into how precisely it makes its profits.

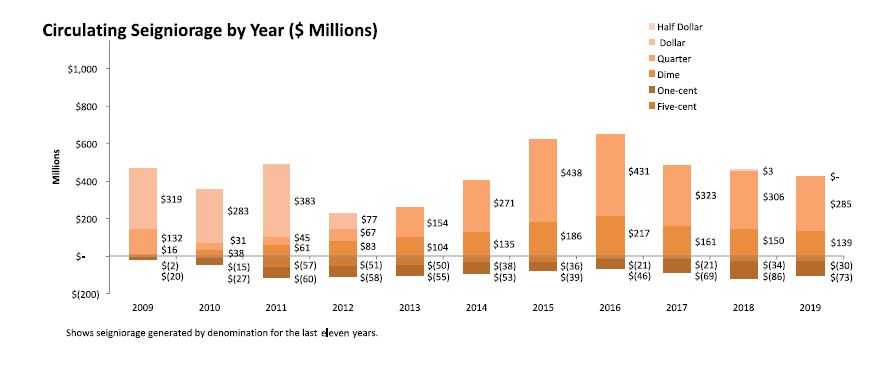

Whereas the quarter is an incredibly profitable coin for the U.S. Mint to produce, other coins are not so profitable. For each one-cent and five-cent coin that it produces, the U.S Mint actually loses money. This is because the cost to produce a one-cent coin is actually 1.68 cents. A five-cent coin costs 6.59 cents to make. The dime is profitable, however. It only costs the U.S. Mint 3.01 cents to make it.

Luckily for the U.S. Mint, the demand for its profitable quarters and dimes far exceeds the demand for its unprofitable nickles and cents. In 2019, the Mint was asked to ship just $73.2 million and $57.6 million worth of nickles and one-cent pieces, whereas dime and quarter shipments were $221.5 million and $445.8 million, respectively.

The U.S. Mint illustrates its coin profitability, sometimes known as seigniorage, in a helpful chart:

The Mint’s seigniorage was at its lowest in 2012, when metal commodity prices were very high. The subsequent decline in prices has helped buoy the Mint’s profit figure. Low metal prices means that it costs less to fabricate circulating coinage.

In conclusion

The big boom in gold and silver coin demand will quickly filter down to the mints. Expect them to quickly ramp up production. Whereas 2015-2019 was a sluggish period for U.S. Mint and the Royal Canadian Mint bullion coin revenues, it looks like 2020 will be a big year. Will it be as booming as 2015? That remains to be seen.

However, the production of gold and silver coins is a low margin business. So even if the U.S. Mint and Royal Canadian Mint enjoy much healthier bullion revenues, this won’t translate into a huge impact on the bottom line. Domestic circulating coins continue to drive an outsized chunk of mint profits, especially in the case of the U.S. Mint.

* It’s possible to get a rough idea about how much the Royal Canadian Mint charges the Department of Finance for coins. In its 2018 Annual Report, the Mint reported $129.3 million net new coins produced for the Department of Finance’s inventory. It also reported receiving $86.7 million in revenue from the Department of Finance. So this implies that the Royal Canadian Mint received 67% of face value from the Department of Finance.

Popular Blog Posts by JP Koning

How Mints Will Be Affected by Surging Bullion Coin Demand

How Mints Will Be Affected by Surging Bullion Coin Demand

Banknotes and Coronavirus

Banknotes and Coronavirus

Gold Confiscation – Can It Happen Again?

Gold Confiscation – Can It Happen Again?

Eight Centuries of Interest Rates

Eight Centuries of Interest Rates

The Shrinking Window For Anonymous Exchange

The Shrinking Window For Anonymous Exchange

A New Era of Digital Gold Payment Systems?

A New Era of Digital Gold Payment Systems?

Life Under a Gold Standard

Life Under a Gold Standard

Why Are Gold & Bonds Rising Together?

Why Are Gold & Bonds Rising Together?

Does Anyone Use the IMF’s SDR?

Does Anyone Use the IMF’s SDR?

HyperBitcoinization

HyperBitcoinization