India's IIBX Bullion Exchange – Price Taker or Price Maker?

Ronan Manly

Ronan Manly 0 Comments

0 CommentsA new government-backed bullion exchange has been established in India, known as the Indian International Bullion Exchange (IIBX). IIBX, which is located in GIFT City in the Indian state of Gujarat, was officially launched on 29 July 2022 by Indian prime minister Narendra Modi.

GIFT City is a new planned business district, positioned half-way between the Gujarat cities of Ahmedabad and Gandhinagar, with ‘GIFT’ standing for ‘Gujarat International Finance Tech’. IIBX is also officially part of India’s new International Financial Services Centre (IFSC) which is located within GIFT City in the GIFT Special Economic Zone (SEZ). The bullion exchange is also regulated by Indian financial regulator the International Financial Services Centre Authority (IFSCA). For an overview of the new IFSC, see here.

Prime Minister #Modi inaugurates India International Bullion Exchange (#IIBX) at GIFT City in Gandhinagar. The #goldexchange aims to facilitate efficient price discovery, ensure standardisation & quality, and become an influencer for global #bullionprices. #GrowthWithGIFT pic.twitter.com/r9go8KCGBh

— CorpIndiaNews (@CorpIndiaNews1) July 29, 2022

In addition to the creation of IIBX having been facilitated by the Indian federal government and the IFSC having been developed by the state government of Gujarat, the holding company which operates the bullion exchange has backing from the private sector in the form of a number of India’s large exchange and clearing type entities. As the IIBX website states:

“Pursuant to Memorandum of Understanding between Central Depository Services (India) Limited (CDSL), India INX International Exchange (IFSC) Limited (INDIA INX), Multi Commodity Exchange of India Limited (MCX), National Securities Depository Limited (NSDL) & National Stock Exchange of India Limited (NSE),

…the holding company India International Bullion Holding IFSC Limited (IIBH) was created for setting up and operationalizing India International Bullion Exchange [IIBX], Bullion Clearing Corporation and Bullion Depository in IFSC, GIFT City.”

You can view the various websites of these entities here – CDSL website, NSDL website, MCX website, NSE website, India INX website (INX is a subsidiary of the Bombay Stock Exchange (BSE)).

Gold Spot contracts and the Vaults

Initially IIBX has listed two spot gold contracts for trading, a 1 kilo Gold contract of 995 fine gold contract, and a 100 gram Gold Mini contract of 999 fine gold contract. Both contracts are denominated in and traded in US dollars. These contracts have same day settlement (T + 0) and settlement is compulsory in the form of a Bullion Depository Receipt (BDR). A BDR is an electronic record representing a unique gold bar held in an IIBX approved vault.

In a 2nd August article about the IIBX launch, India’s Economic Times said that “IIBX has three vaults at GIFT City where 446 tonnes of gold and 2,580 tonnes of silver can be stored”. Where these 3 vaults are and who runs them is not clear, since on the IIBX website, there is a ‘vault directory’ page but it only lists one vault, which is located at “Ground Floor, Pragya Tower, GIFT SEZ, GIFT City, Gujarat”, with the vault manager stated as being “Sequel Logistics Pvt Ltd”. On its website, Sequel describes itself as “India’s largest secure logistics network”.

Note – this “Pragya Tower" is the same building that the IFSC Authority lists as being its headquarters – the IFSCA is on the 2nd and 3rd floors of Pragya Tower. The IIBX company (India International Bullion Exchange IFSC Ltd) is located next door to IFSCA, on the 13th floor of the “Brigade International Financial Centre". Looking at satellite images of GIFT City, it appears a lot of the planned buildings have yet to be built.

In a Bloomberg video interview on 29 July, the IIBX CEO Astok Gautam says that the IIBX “has international vaulting partners“. In another coverage article of IIBX on the Ahmedabad Mirror website, the IIBX CEO is quoted as saying that “Three gold vaults have been constructed in Gujarat due to IIBX”. But three vaults in the Indian state of Gujarat is not necessarily the same thing as “three vaults at GIFT City” as the Economic Times stated.

According to the IIBX contract specifications for both the 1 kilo and 100 gram gold contracts, the gold bars backing the contracts “should be serially numbered gold bars supplied by LBMA approved suppliers or other suppliers as may be approved by IIBX to be submitted along with suppliers quality certificate.”

As to what exactly a “LBMA Approved supplier" is, the IIBX does not say. If it had said “LBMA approved refiners" then that would be more logical as it would tie in with the LBMA Good Delivery Lists. As it is, “LBMA Approved supplier" could include LBMA banks, but maybe the point is mute anyway, since IIBX will be able to approve “other suppliers" anytime it wants to.

Congratulations to Prime Minister @NarendraModi on launching India International Bullion Exchange (IIBX) and the NSE IFSC-SGX Connect – the latest phase of growth at GIFT City. These ambitious initiatives will help drive a new generation of Indian economic growth.

— Mike Bloomberg (@MikeBloomberg) July 29, 2022

Direct Imports – Without the Banks?

One major benefit being touted by IIBX about the new bullion exchange is that it will allow Qualified Jewellers (as approved by the IFSCA) to directly import gold into India, by allowing Qualified Jewellers to trade gold contracts on the IIBX exchange and then take delivery of these contracts.

As one of the world’s largest importers of gold (India officially imported 1,067 tonnes of gold in 2021), this change should add more price transparency to the Indian gold import process, because up until now, only authorised banks and authorized agencies have been permitted to import gold into India.

Authorised Dealer (AD) banks are banks nominated and approved by India’s central bank, the Reserve Bank of India (RBI). Authorised agencies are entities that are authorised by the Directorate General of Foreign Trade (DGFT) of the Indian Department of Commerce, and include India’s large trading companies known as Public Sector Undetakings (PSUs).

These PSUs include the massive conglomerates such as Metals and Minerals Trading Corporation of India (MMTC), State Trading Corporation (STC), Projects & Equipment Corporation of India (PEC), and Handicraft and Handloom Export Corporation (HHEC). See the BullionStar Gold University article on India for an explanation of these authorised agencies.

But now with the opening of the IIBX, Qualified Jewellers will be able to import gold into India via the IIBX. As per an RBI Circular, dated May 2022:

“…in addition to nominated agencies as notified by RBI (in the case of banks) and nominated agencies as notified by DGFT, Qualified Jewellers (QJ) as notified by the International Financial Services Centre Authority (IFSCA) will be permitted to import gold under specific ITC(HS) Codes through India International Bullion Exchange IFSC Ltd. (IIBX)”

These ITC(HS) (trade category) codes are 7108, 7113, 7114 and 7118 – which relate to gold and other precious metals in various forms. The DGFT/IFSCA has defined “Qualified Jewellers" as those companies who a) are engaged in the business of precious metals, i.e. goods under the above ITC(HS) codes, b) have 90% of their turnover in the last 3 years derived from precious metals, and c) maintain a company value of, at a minimum 25 crore in as per their latest audited financial statements. In India a ‘crore’ equals 10 million, so 25 crore equals 250 million rupee.

According to the IIBX website, there are already 64 Qualified Jewellers accepted on the Exchange. As of the time of writing, these 64 jewellery companies were listed on the IIBX list of Qualified Jewellers here, and those familiar with the Indian bullion market may recognise some of the names on the list such as MMTC-PAMP, Riddisidhi Bullions, Malabar Gold, and Titan Company.

However, to trade on the IIBX, Qualified Jewellers must be a Limited Purpose Trading Member (LPTM) or a client of a Bullion Trading Member. As per a 5 August circular from IIBX’s regulator, the IFSC Authority (IFSCA):

“11. At present, a Qualified Jeweller is being permitted to purchase Bullion Depository Receipt (BDR) on IIBX -only for import of gold, either as a client of a Bullion Trading Member or as a LPTM. The option for a Qualified Jeweller to access IIBX as a Trading Member is currently not operationalized and shall not be available.”

Currently, there are only 13 Member companies of the IIBX, all of which appear to be domestic companies and all of which have registered addresses in the same building (Signature building) in the GIFT SEZ. See list here.

Very surprisingly, Qualified Jewellers cannot sell gold on the IIBX, as the IFSCA Circular says that:

“The Qualified Jewellers shall only be permitted to purchase BDR on IIBX towards import of gold and shall not in any manner be permitted to enter a sell order or cancel the purchase order.“

This does not seem like an efficient market for price discovery if the Qualified Jewllers are only allowed to enter buy orders for gold but are prohibited from entering sell orders for gold. Perhaps the Qualified Jewellers will be allowed to trade and exchange Bullion Deposit Receipts (BDRs) among themselves on the IIBX. However, this is not discussed on the IIBX website nor in Indian media coverage, nor even in the IIBX Vault Manager’s Standard Operating Procedures.

Price Discovery or mere Price Transparency?

Not surprisingly, the vested parties to the IIBX all claim that trading gold on the Indian International Bullion Exchange (IIBX) will lead to better price discovery, but then again, they would say that.

IIBX’s CEO says “the bullion exchange is the first such transparent platform where jewellers can directly put up bids to import physical gold, leading to better price discovery.“

The press release published by the IFSC Authority (IFSCA) on 29 July to coincide with the launch of the IIBX by Indian PM Modi says that the IIBX has been established “with the vision of making India an influencer of global bullion prices” and that the new bullion exchange:

“will facilitate efficient price discovery and ensure standardisation, quality assurance and sourcing integrity in addition to providing impetus to financialisation of gold in India.”

But given that global bullion prices are in reality established via the nearly unlimited trading of fractional unallocated LBMA paper gold in London and by enormous cash-settled gold futures trading on the US COMEX, the goal of India’s IIBX in influencing global bullion prices (international price discovery) is not something that could ever be achieved in the short term, and only then if the entire structure of global gold price discovery is taken out of the hands of the LBMA bullion banks.

Even India’s Economic Times agrees with us on this, so maybe the IIBX backers know this also. In a 4 January 2018 article in the Economic Times, Aasif Hirani wrote that:

“recent research shows gold prices are derived from London Over-the-Counter (OTC) spot gold market trading and COMEX gold futures trading. It means international gold prices are set by paper gold market, and not by physical gold market.

One should understand that supply and demand for physical gold plays no role in setting the gold price in COMEX and London OTC market."

The Economic Times article was even so kind as to quote BullionStar, saying that:

“According to BullionStar.com, the London OTC market predominantly involves trading of synthetic unallocated gold, meaning trades are cash settled. COMEX is a derivative market, where gold is traded in futures and 99.95 per cent of trades are settled in cash.

Only one out of 2500 gold futures contracts is settled in delivery. Even less physical gold is delivered to COMEX warehouse and even less gold is withdrawn from it."

More locally, what the IIBX looks set to do in the short term is to partially disintermediate the banks and authorised agencies that up until now have had an exclusive right to import gold into India. Under the status quo model, the banks and authorized agencies source gold from international suppliers (including international banks) and then import the gold into India on a consignment basis (where they get paid to store it), before supplying it to jewellers and dealers at a markup.

With Qualified Jewellers now allowed to bid for gold on the IIBX and enter the price they want to pay the seller, this should in theory allow the prices established to the exchange to be

a) more efficient than they would have been in a bi-lateral deal between an importer and a jewellery company, and

b) more transparent than the previous opaque system because the IIBX traded prices will now be public for anyone to see

In an article dated 2 August, and titled “Bullion Exchange set to aid India’s forex“, the The Economic Times quotes “people familiar with the matter" who claim that trading on the IIBX could reduce gold import costs “by as much as $50 a kilogram initially“. So that for every 100 tonnes of gold imported via the exchange, “jewellers could save up to [US]$ 5 million in forex“. With India officially importing up to 1000 tonnes of gold per annum (excluding gold smuggling), if the IIBX took a 50% share of this import flow, that would work out at US $ 25 million that the jewellers in total could save by not ‘directly’ using the importing banks.

But the pricing action, and the potential savings in not paying what the importing banks previously quoted will depend on the power of the buyers (who will now be more concentrated on the exchange) versus the power of the sellers.

Presumably, the sellers will still include the domestic branches of the banks and the authorised agencies who previously imported gold, but could also include specialist gold brokers, and international sellers directly accessing the exchange. So will the sellers try to maintain the status quo by trying to quote prices in the same way that they previously did when they negotiated import prices directly with the Indian jewellery companies? You would think, yes, they will try to do this.

Bullion Banks – The Usual Suspects

Also as expected, the big bullion banks (LBMA banks) will not take kindly to a new gold exchange and a potential new pricing mechanism existing unless they are involved. As the IIBX CEO in the same video interview with Bloomberg (minute 2:11) said, the international bullion banks are already on their way:

“we expect international foreign bullion banks, the big bullion dealers, they are already in talks with us, many of them have already started inquiring, a few have already joined as clients of our trading members, and they look forward to starting to come here and start using our facilities for supplying gold.”

The Economic Times also claims that:

“[IIBX] is sourcing physical gold from top global bullion banks. JP Morgan, Citi, Standard Chartered and ICBC are among likely institutions that either supplied physical gold or are in talks to do so."

But prohibiting the Qualified Jewellers from selling gold on the Exchange is definitely an impediment to liquidity, as it reduces liquidity, keeps the selling in the hands of the previous sellers, and also prevents Qualified Jewellers from selling gold to each other. An important question is can the Bullion Despository Receipts (BDRs) which back the gold in the IIBX vaults be traded (bough and sold at will) by Exchange Members and clients of Members?

Ashok Gautam, IIBX CEO, says yes. Again, in the Bloomberg video interview (minute 3:10), Gautam explains the trading of BDRs (with cross-talk from the Bloomberg interviewer lady trying to butt in):

“These BDRs can be actively traded, you can sell the BDR and take your dollars out, and you can also convert the BDR to physical metal, and take the gold or silver out without any hassle."

Red Tape – Indian Style

Sounds neat, but the Qualified Jewellers still face a lot of central bank and government bureaucracy and red tape in even making a purchase order on the IIBX, and worryingly, the whole process still involves commercial banks. According to the IFSCA 5 August Circular, once a Qualified Jeweller has put in a buy order, IIBX then has to issue:

“an IIBX authenticated document carrying details of indicative price of gold for the quantity and the quality(purity), intended to be imported by the Qualified Jeweller through IIBX"

This document is then used as the basis:

“on which an Authorised Dealer (AD) bank may allow Qualified Jewellers to remit advance payments towards [the] import of gold through IIBX"

So the banks are still involved, and the Qualified Jewellers have to transfer advance payments to the banks.

A Reserve Bank of India (RBI) Circular from 5 May 2022 has even more details of this bureaucracy. Very quickly, what it says is that the AD banks “may allow" the Qualified Jewellers “to remit advance payments for eleven days for import of Gold through IIBX in compliance to the extant Foreign Trade Policy and regulations issued under IFSC Act.“

The AD banks have to check that the amount sent by the jewellers matches “the terms of the sale contract" and the banks have to carry out due diligence on the remittances of the Qualified Jewellers. The Qualified Jewellers also have to “submit the Bill of Entry … issued by Customs Authorities to the AD bank from where advance payment has been remitted.“

In short, for the Qualified Jewellers to place a buy order on the IIBX, there are still a whole host of rules involving the RBI, the IFSC Act, the banks, the Department of Commerce (DFTG), and the customs authorities. But in a market which was even more inflexible and the jewellers had to accept 30 day consignment periods and high fees from the banks, maybe they think the IIBX is a game changer, i.e. could it be a case of ‘the previous system was so atrocious that any improvement that the IIBX can bring is welcome"?

Conclusion

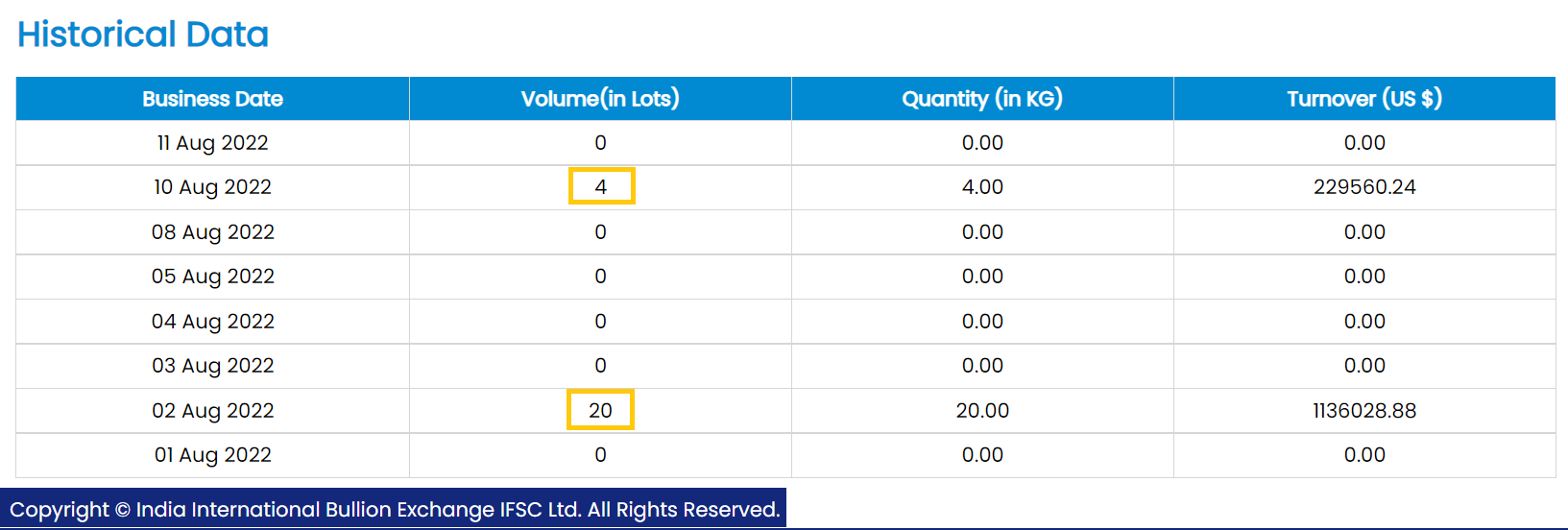

Trading of the new IIBX gold contracts has been very thin so far with only 24 kgs being traded (i.e. 24 lots of the 1 kg contract). A full 20 of those lots were traded on 2 August and 4 lots were traded on 10 August. See screenshot above. The quoted turnover figures in US$ show that that prices being quoted are in and around the international spot price in US dollars. For example, the 4 kgs traded on 10 August for a US$ turnover of 229,560.24, equates to $1794 per troy oz, which was very near the LBMA Gold Price AM fix that day of $1793.50.

Sure, the new IIBX will probably improve standardisation of the quality of bullion imported into India and will probably improve responsible sourcing, but will it allow India to become a Price Taker?

The IIBX CEO concludes his interview with Bloomberg saying that “India will slowly but surely emerge as a pricing influencer in the gold market”. Likewise, in his speech at the launch of IIBX, Indian prime minister Modi said that “India’s identity should not be limited to just a big bullion market but it should be recognised as a ‘market maker’." These sentiments are all very well and a nice vision, but with the international cartel of viper bullion banks invited to the IIBX party, is that really going to happen?

Unfortunately, not unless the paper trading games of the LBMA and COMEX fall apart. But perhaps what the IIBX is doing, in the same way as China’s Shanghai Gold Exchange, and Dubai’s DGCX, and Turkey’s Borsa Istanbul, is establishing spot gold contracts and the associated trading and vaulting infrastructure for a gold exchange, in preparation for a time in the future when the paper gold market implodes, and as GATA’s Bill Murphy says, the bullion banks are “taken out on a stretcher“.

Popular Blog Posts by Ronan Manly

How Many Silver Bars Are in the LBMA's London Vaults?

How Many Silver Bars Are in the LBMA's London Vaults?

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

German Government Escalates War On Gold

German Government Escalates War On Gold

Polish Central Bank Airlifts 8,000 Gold Bars From London

Polish Central Bank Airlifts 8,000 Gold Bars From London

Quantum Leap as ABN AMRO Questions Gold Price Discovery

Quantum Leap as ABN AMRO Questions Gold Price Discovery

How Militaries Use Gold Coins as Emergency Money

How Militaries Use Gold Coins as Emergency Money

Hungary Announces 10-Fold Jump in Gold Reserves

Hungary Announces 10-Fold Jump in Gold Reserves

Planned in Advance by Central Banks: a 2020 System Reset

Planned in Advance by Central Banks: a 2020 System Reset

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets